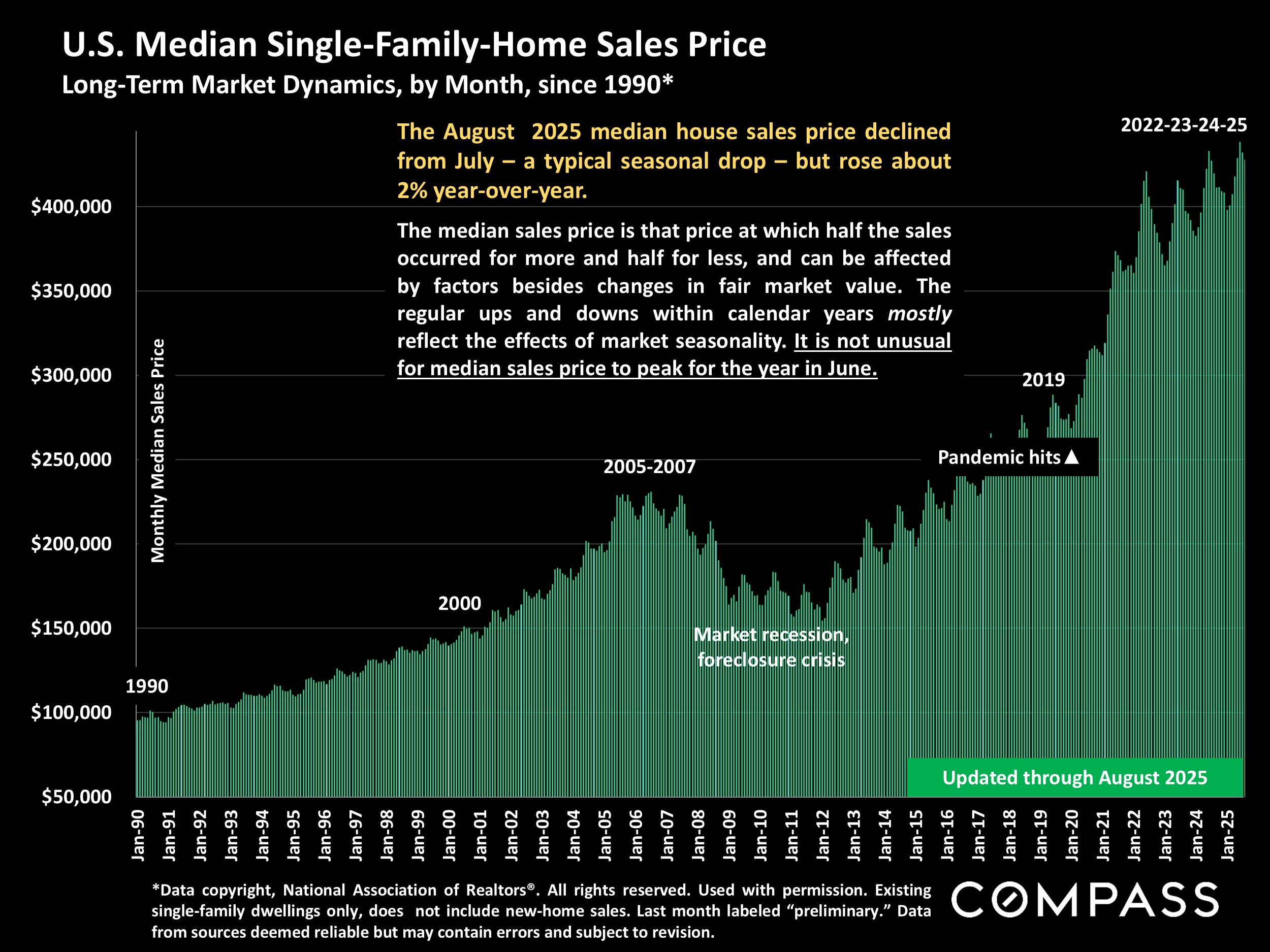

The median existing-house median sales price continued to rise on a year-over-year basis, as did the median condo/co-op price. One factor - in addition to general appreciation trends - is that affluent buyers, purchasing more expensive homes, have been playing an increasing role in demand since stock markets began soaring in early 2024. This helps pull median sales prices higher.

The number of new listings coming on market has substantially declined from the multi-year high reached in April 2025, but was still 5% higher year over year in August.

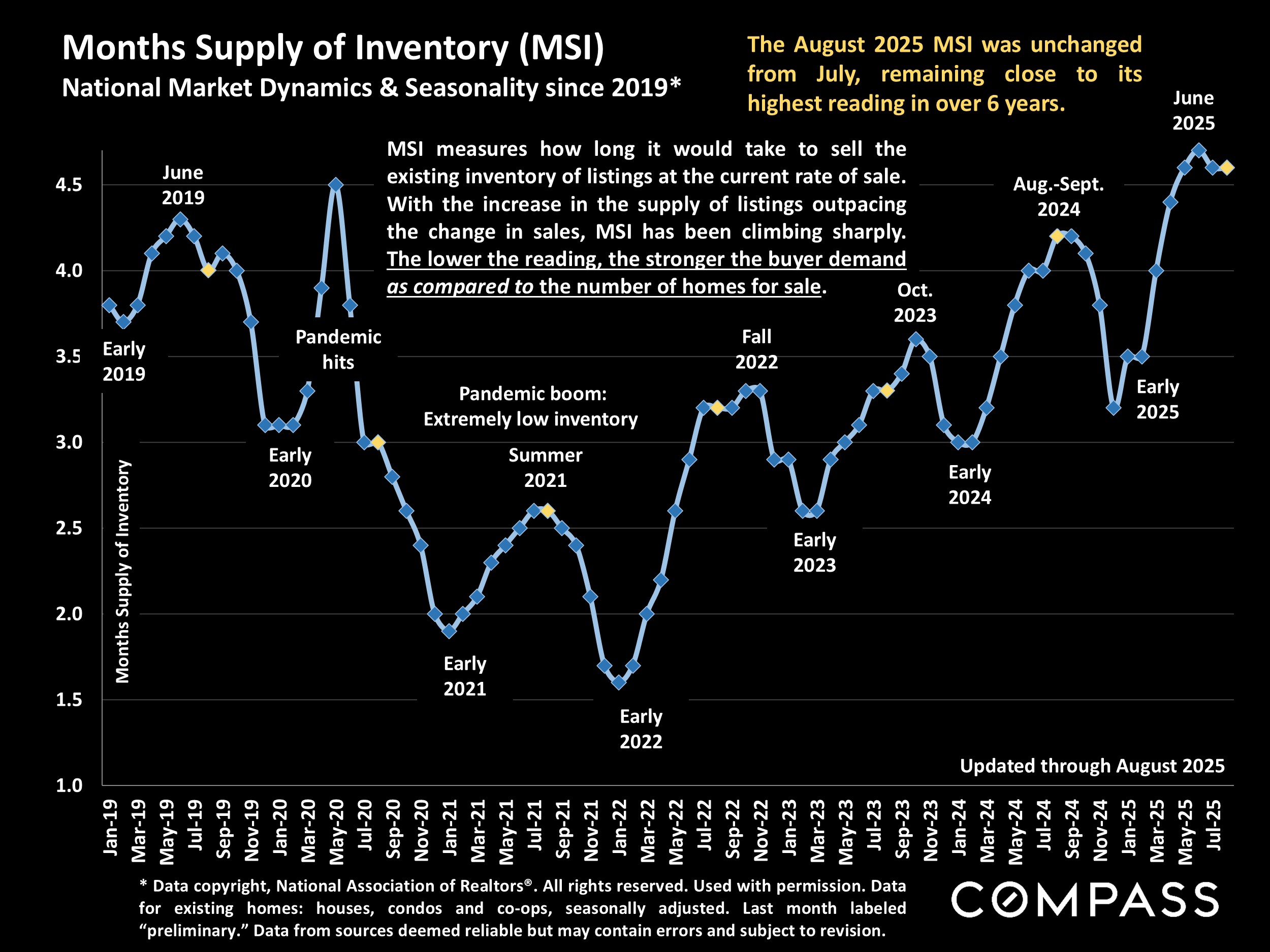

Months-supply-of-inventory (MSI) compares buyer demand to the supply of homes available to purchase. The lowest readings, such as during the pandemic boom, signify heated seller's markets, while higher readings favor buyers. With the substantial year-over-year increase in inventory amid a relatively flat level of demand, MSI in recent months has been running at a 6+ year high. As with virtually all real estate statistics, MSI also rises and falls to seasonal supply & demand trends.

The 12-month-rolling average of home sales is a broad measurement useful for illustrating long-term trends, and by that calculation, the number of sales has been bumping along at a very low count similar to the great recession. Hundreds of thousands of homes still sell every month - many sell very quickly for over list price - but pricing, preparation and marketing are currently of vital importance for sellers.

The weekly average 30-year mortgage rate ticked up slightly after the Fed cut its benchmark rate on 9/17/25, but remained well below rates prevailing since 2025 began. Where it goes from here will play a major role in the fall selling season.